Southern California Ports Have Regained Their Growth Footing, But West Coast Gateways Still Have a Heavy Lift to Full Recovery

By Mike Jacob, President, Pacific Merchant Shipping Association

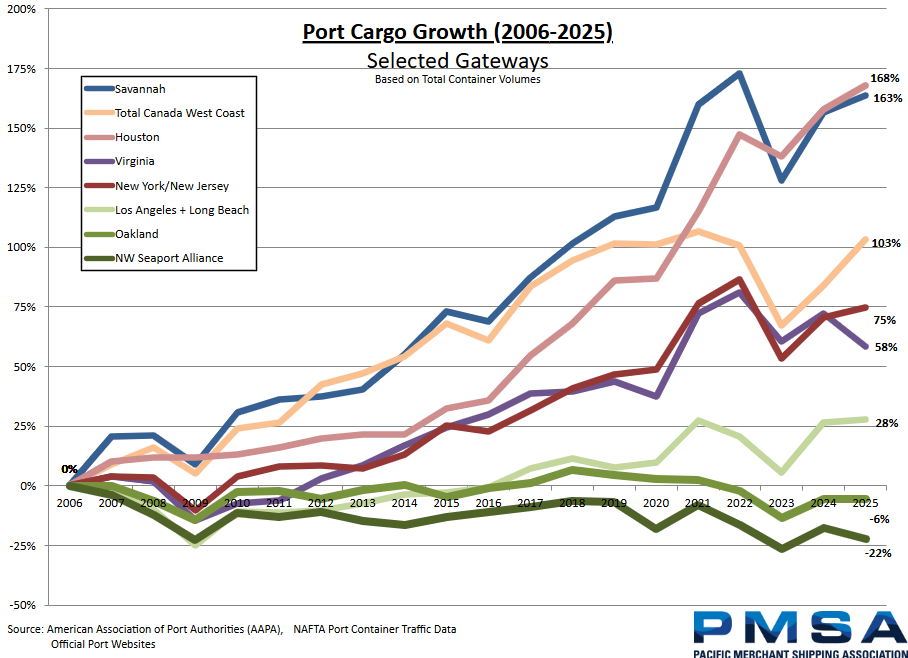

Two decades ago, U.S. West Coast ports commanded a growing, dominant share of the nation’s containerized trade. Sitting in the trade lanes where the demands of the world's largest consumer economy met the rapidly maturing supply of China's ascendant global manufacturing leadership, many predictions of future West Coast traffic were essentially just linear growth projection without interruptions. Our Ports were ascendent. By 2025 U.S. West Coast container volumes hit 24,682,917 TEUs, with a total marketshare of all North American container traffic peaking at 48.1%.

But the West Coast’s inability to recapture Great Recession recovery volumes made it obvious we had slept on our prior advantage. The intermodal, discretionary cargo market steadily became more competitive after trade volumes everywhere started their recovery after 2010. But we embraced other priorities than revenues, volumes, and competition.

Other gateways got smarter, invested in new port terminals, and built and created large distribution center nodes and intermodal upland properties, but California in particular, went on a unique, cost-inducing bender. The collective cost of early goods movement emissions controls adopted in 2007-2009, based on pre-recession projections of unlimited future growth, ultimately drove an additional $5 billion in costs of doing business that our competition did not have. And these new costs and heavy lifts of new regulatory paradigms were occurring precisely when cargo owners were making decisions about when and where to re-establish their IPI cargo routing. The diversions, logically, accelerated.

By 2019, the volumes diverted from West Coast gateways reached some 5.6 million TEUs in that year alone. Not lost to lower demand by American importers and exporters, but -diverted to other gateways like Houston, Savannah, Virginia, or the Canadian gateways at Vancouver and Prince Rupert.

The opportunity costs of these losses are hard to overstate. In a recent report focused exclusively on Southern California, the local and state economy suffers directly when volumes are lost. Regional employment has been reduced by approximately 77,000 jobs per year, and cumulative losses to the regional economy since 2006 as a result of diversion are an estimated $77.4 billion.

So, while we very heartily celebrate the headline volume numbers out of Southern California from 2024 and 2025, the celebration represents only the stabilization of a trend reversal for Los Angeles and Long Beach. We have officially put the brakes on the Southern California slide, but we still have a lot of work to do and a lot of volumes to recapture from our competitors.

For starters, even by stabilizing the market back to and exceeding 2019 volume levels, the LA and LB gateway lives in the shadow of its context. To truly recover and regain our competitive dominance, we need to invest in every and all efforts to recapture the discretionary cargo that has left, and the missed growth volumes that were projected to accrue on top of those base volumes.

This is a tall order, and it won’t be easy, but total volume growth and recovery is the most important competitive challenge facing the entire U.S. West Coast today.

First, while LA and LB may be back on competitive footing, this only represents the opportunity to recapture cargo – it has not come back yet. As of July 2025, U.S. West Coast ports held just 37.2% percent of U.S. containerized import tonnage.

Against that backdrop, the Ports of Los Angeles and Long Beach have had a genuinely impressive run from 2019 to 2025. Through last year, the San Pedro Bay complex moved 20.12 million TEUs, an increase over pre-pandemic 2019. These are record volume setting years where we have moved the same amount of cargo as during the peak of the pandemic, but without congestion. This high efficiency, low dwell times, and peak environmental progress performance should be recognized for what it is: proof that world-class competitive performance is possible in Southern California. This has not been easy, it required high levels of performance from ocean carriers and marine terminal operators and all of our supply chain partners.

But it’s just the first step.

Southern California is, and will remain, the largest gateway in North America. We are proud of this record and, despite the competitive attrition, we still hold the volume crown. The questions are how much and how fast we can truly capitalize on opportunities to compete and recapture a meaningful share of the intermodal cargo that left.

But the entire West Coast is still behind the marketshare eight-ball. Houston, Savannah, and the Port of Virginia all posted stronger 2025 year-to-date volumes than any U.S. West Coast complex. And much of the cargo they are moving remains discretionary transpacific intermodal freight that, on the merits of transit time and logistics cost, still logically should prefer the Pacific gateways.

Our path back to competitive parity with Gulf and East Coast gateways runs through Southern California and starts with continued investment in terminal capacity, landside intermodal connectivity, and the kind of regulatory predictability that allows shippers and carriers to make long-term routing decisions with confidence. Every time cargo owners choose an alternative gateway over a West Coast port is a moment that inland distribution networks reorient, and the friction and cost of returning rise. The lesson we learned over the past two decades is that the window to compete for that cargo does not stay open indefinitely.

This is also important because a meaningful share of Southern California growth was not recapturing discretionary cargo from the Gulf and Atlantic coasts, but consolidation of West Coast volumes. For example, the Port of Oakland has shed roughly 210,000 TEUs from its 2019 baseline, a 10% decline. The Northwest Seaport Alliance has lost approximately 550,000 TEUs, down 17% from its pre-pandemic 2019 high. Together, Oakland and Puget Sound have shed 760,000 TEUs since 2019, which represents nearly 30% of Southern California’s gain over the same period. The picture that emerges is of a West Coast system that is also redistributing cargo internally, rather than recapturing it from the competitors that were sapping overall growth from the system.

This only adds to the investment imperative. Southern California’s record volumes should motivate, total commitment to new West Coast competitiveness, and renewal of broader competition. And the San Pedro Bay ports have demonstrated what the bedrock for improved competition looks like: the avoidance of costly, local regulatory proposals that would have burdened terminal operations or imposed cargo caps, combined with a renewed commitment to intermodal infrastructure investment. These are the points that will further move us in the right direction.

The bottom line is that in 2005, at peak marketshare, we moved 24,682,917 TEUs on the US West Coast. In 2025, we moved 25,531,488 TEUs. We have sacrificed 20 years of growth already, at tremendous expense. We cannot afford to miss this opportunity to invest, compete, build, and grow again.